Cases of White Claw on display in New York

Is hard seltzer here to stay or will sales of the fizzy alcoholic water eventually go flat? That’s the question beer industry observers have been asking for much of 2019.

Similar to conversations about where hard soda was headed of a few years ago, there are opinionated stakeholders – some armed with data to strengthen their arguments — on both sides of the debate.

If you ask Sanjiv Gajiwala, the vice president of marketing at Mark Anthony Brands, makers of White Claw, he’ll tell you how bullish he is on the future of the segment and he’ll back it up with some compelling statistics.

“I think that if hard seltzer was like hard soda, you would have seen a splat earlier this year,” he told me in September, noting that sales have grown 300% in each of the last four years.

According to Gajiwala, a key indicator of the long-term potential for hard seltzer are repeat purchase rates.

“Less than one out of ten consumers that bought a hard root beer, bought it again a second time,” he explained. “Over 30 percent of consumers who buy White Claw once, buy it again. That doesn’t sound like a splat to me.”

Another reason for hard seltzer makers to be optimistic? Less than 9% of American households have purchased one, compared to about 70% of U.S. households that buy beer.

“As you start to think about that opportunity, I think we feel pretty bullish about the future of the brand,” he told CNN last month.

Of course, there are those who believe today’s hard seltzer drinkers will eventually tire of the product and return to other beverages. Longtime beer writer Jeff Alworth has called the hard seltzer boom a “fad,” and he believes soaring sales will eventually level off.

“They’re fundamentally uninteresting, and when the novelty wears thin, so does the trend as a national force,” he wrote earlier this month.

That’s a far more subjective spin on the current level of consumer interest in these products, but his argument is that hard seltzer is simply a small niche within the broader beer category.

That might be true for now – more than 82 million nine-liter cases of hard seltzer will be sold in 2019, according to IWSR, a data firm that provides insights on the alcoholic beverage market.

By 2023, however, sales of hard seltzer are expected to more than triple to over 281 million cases, IWSR predicts.

“Hard seltzers are far from a fad, they’re growing at a spectacular rate, and increasingly, hard seltzer producers are pulling consumers from other beverage alcohol categories, not just beer,” IWSR chief operating officer Brandy Rand said via a press release.

IWSR recently compiled a comprehensive report on the state of the hard seltzer market, which it claims is now larger (by volume) than the leading spirits category – vodka.

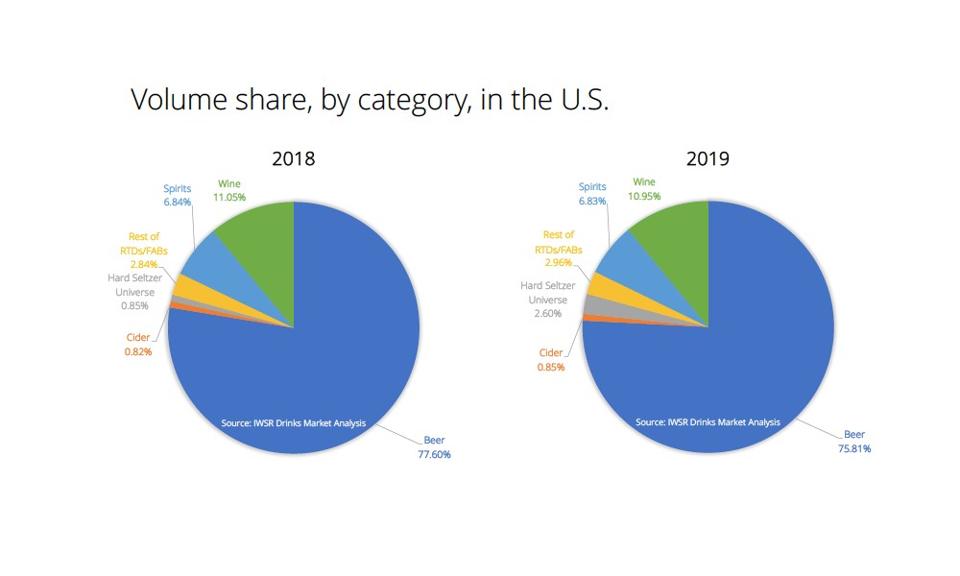

Hard seltzer products – including those made from a wine or spirits base — now control about 2.5% of the entire U.S. alcohol market, according to IWSR, and Rand believes is becoming its own category.

“Consumers don’t look at White Claw or Truly as being a part of the beer category,” she told me.

White Claw and Truly (owned by Boston Beer Company) control approximately 85% of the hard seltzer market, according to investment firm Guggenheim Partners, but dozens of smaller players have introduced their own offerings this year.

“You’re going to see all of these brands that are in cans – some malt-based, some wine-based and some spirit-based – all stacked together,” she added. “To a consumer, they’re all canned refreshment with flavors.”

IWSR sized up the U.S. alcohol category and found that hard seltzers would make up 2.6% of volume in … [+]

Rand makes an important point about refreshment: Hard seltzer appeals to male and female consumers who normally drink wine, beer and spirits offerings.

Earlier this year, Gajiwala told me that 55% of White Claw’s volume was coming from beer, while 20% was coming from wine and 17% from spirits. The remaining 8% is being sourced from other cider and flavored malt beverage products, he said.

According to Brewers Association chief economist Bart Watson, who analyzed sales data from research firm IRI earlier this year, only 27% of hard seltzer volume is being sourced from beer.

“The rest is either coming from getting new drinkers into beverage alcohol, or from increased purchases that are incremental to existing off-premise sales,” he wrote in October.

However, Watson noted that per capita alcohol consumption historically hasn’t changed much over time – legal drinking age Americans consume about 2.5 gallons of pure ethanol each year, according to National Beer Wholesalers Association chief economist Lester Jones — so hard seltzer sales are not purely incremental.

Nevertheless, hard seltzer drinkers spend an average of $219 more on adult beverages annually compared to the average alcohol-buying household, according to Nielsen, and 40% of hard seltzer buyers are repeat customers.

Meanwhile, numerous beer industry executives I’ve spoken to in recent months have expressed concerns that hard seltzer sales could accelerate light lager declines; sales of Bud Light and Coors Light, the largest individual U.S. beer brands, are both down 5.8% and 2.9%, respectively, according to IRI.

One regional brewery owner in the Southeast recently told me that that large chain retailers are planning to reduce shelf space for craft beer in order to make room for hard seltzer SKUs. If that’s true, those outlets would be wise to consider that craft beer drinkers are two times more likely to purchase hard seltzer than the average drinker, according to Nielsen.

So just how big is the hard seltzer category today?

According to Nielsen, hard seltzer sales at off-premise retail stores reached $1.3 billion over the 52-week period ending November 2, 2019. During that span, drinkers spent more on hard seltzer than they did on sauvignon blanc ($980 million) or craft beer 12-packs ($1.2 billion), the firm reported.

Interestingly, sales of hard seltzer are also sneaking up on the craft beer’s largest individual style: IPA. According to Nielsen, off-premise sales of craft IPAs reached $1.5 billion during the above-mentioned 52-week period. However, Gajiwala told CNN last month that sales of White Claw would surpass $1.5 billion in 2019, and that category-wide sales would approach $2.5 billion.

Maybe boozy water is going to be a bit of a bogeyman for beer after all.